|

| ?action=logout">Log out |

|

|

|

March 12, 2008

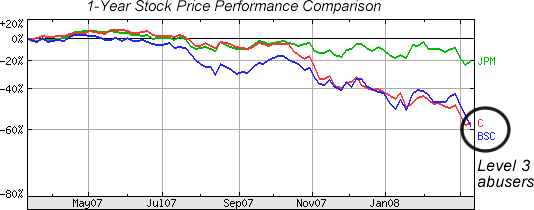

I note the term level 3 dreams because these assets are not readily tradable and their value is whatever the company thinks it is. Using Citigroups 10K, here is the breakdown of these asset classes: Level 1Quoted prices for identical instruments in active markets. Level 2Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations in which all significant inputs and significant value drivers are observable in active markets. Level 3Valuations derived from valuation techniques in which one or more significant inputs or significant value drivers are unobservable. For a more in-depth summary of some of the assets logged as level 3, a quote from Bear Stearns will suffice: Level 3 is comprised of financial instruments whose fair value is estimated based on internally developed models or methodologies utilizing significant inputs that are generally less readily observable. Included in this category are distressed debt, non-performing mortgage-related assets, certain performing residential and commercial mortgage loans, certain mortgage- and asset-backed securities and residual interests, Chapter 13 and other credit card receivables from individuals, and complex derivative structures including long-dated equity derivatives. Turning to the Fed, yesterdays announcement of a new $200 billion Term Securities Lending Facility is being hailed by some as wonderful news in that it will help stressed financial players borrow more capital for a longer period of time using crappier assets as collateral. Calling this program a historic innovation, Business Week concluded the following: The Term Securities Lending Facility (TSLF)announced Mar. 11is a more powerful and more precise tool for addressing the dislocations in the credit market. It is aimed at the heart of the current problems: mortgage-backed securities. The problem is that nobody knows what these complicated securities are really worth, so they are clogging up bank balance sheets and impeding the normal flow of credit. Without getting into technical details, the TSLF elegantly sidesteps the problemthe big banks can use these securities as collateral, and borrow Treasuries from the Fed. The intended result: more lending and borrowing, as nature intended. While the Feds newest lending program could certainly help some financial players or at least allow bad assets to fester on their balance sheets - the very idea that more lending and borrowing is what is required to solve the current crisis may be wishful thinking. Quite frankly, if the three companies mentioned above already have extremely stressed balance sheets, isnt their added risk in awarding these players the chance to essentially trade out of their losses? Using the 1990s lesson of Japan, would it not be preferable for the Fed to compel financial market participants to write-off bad debts and sure up their balance sheets rather than encourage even more risk taking using what could be toxic assets as collateral? Ahh, but here is the rub: if the Fed stands idly by while level 3 dreams come crashing down the credit crunch will almost surely worsen, many market participants could go bankrupt, and this could put the entire U.S. financial system at risk. Needless to say, what really compounds the rouge balance sheet problem for the Fed is that the pool of potential borrowers is quickly shrinking as the balance sheets of American households start to deteriorate. Using last weeks data, for the first time since the stock market bust household net worth declined in 4Q07. In other words, the great U.S. housing bust is not yet complete, financial companies are already severely stressed, the average U.S. consumer is increasingly less capable of borrowing more, and Fed rate cuts have failed to ease lending standards. If your response to this complex set of issues is make money cheaper and more readily available to the lenders!, you could be Fed boss

|