|

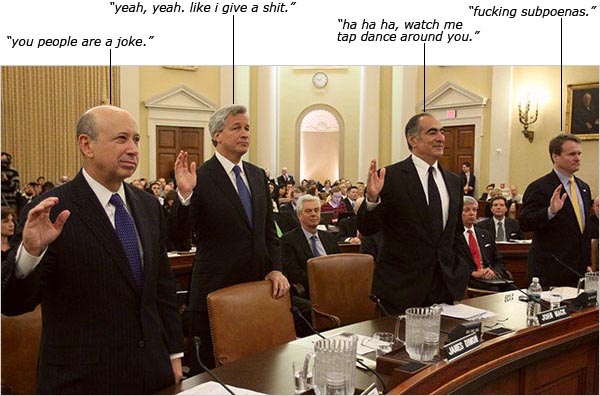

The Financial Crisis Inquiry Commission began operations last week and heard testimony from four heads of the financial industry. Not surprisingly, the tone was resoundingly negative - Inquiry Chairman, Philip Angelides, attacked Goldmans Lloyd Blankfein, Krugman called the bankers clueless, and Ritholtz posted a graphic depicting what was really on the minds of the sleazy bankers. Also not surprising was that no one made the case that what these bankers did was illegal and/or prosecutable.

If you start from the position that the bankers didnt break the law you eventually arrive at the conclusion that the laws must be changed. After all, if Goldman can package and sell toxic assets that are rated triple-A while at the same time purchasing insurance just in case these assets blow-up, something is seriously amiss. For that matter, if the banks are permitted to report multiple interpretations of assets, and off balance sheet shenanigans persist, transparency is basically non-existent. New (or at very least the enforcement of old) regulations are clearly required to limit needless innovation and bring back accountability, to dramatically increase transparency in accounting, and to ensure that no single market or market participant can put the entire system at risk.

But instead of pushing towards these types of ambitious regulatory goals, the narrative of good and evil continues to be evoked (with Wall Street epitomizing evil and, apparently, everyone else representing the good). It is this radical polarization and the more general pre-occupation with levying blame for yesterdays financial crisis that has spawned an ominous reticence insofar as attacking those charged with trying to prevent tomorrows financial crisis.

If a football team performs badly there is a brief period where the concept of blame is debated (i.e. the general manager takes a couple days to blame everyone but himself and then he fires the coach and shakes up the roster). Roughly 2-years into the financial crisis and absolutely nothing has been done to change the system: the same players take to the same field every trading day, a largely toothless reform packages sits in the Senate waiting to becoming even more toothless, and Obamas politically driven bank tax borders on the pointless. The end result is that when Blankfein and others throw a touchdown (by legally speculating in the financial markets) the crowd is left yelling in vain - hes still a bum!

What About Ex-Homeowners?

I put a $400,000 for sale sign on my house and immediately received offers for $550,000 and $585,000. Knowing that the house really wasnt worth that much I informed the first bidder the house was his for $400,000

No one expects individual homeowners to operate like this, so why do we expect this of Wall Street?

Many average homeowners thought they had become sophisticated real estate speculators during the bubble years. Few were right. Many homeowners also stretched the legal boundaries when filling out their mortgage application(s) and blissfully amassed reckless amounts of leverage as home prices increased year-after-year (we know how this worked out). Finally, during the bubble days if many U.S. homeowners could flip a house to a naïve homebuyer with more credit than common sense they gladly would. With these facts known, why are homeowners not being grilled in front of the Financial Crisis Inquiry Commission?

Of course those damn greedy bankers got bailed out and are paying themselves huge bonuses while homeowners across America suffer. Nevertheless, Wall Street has almost fully compensated the taxpayer for their bailout, while the U.S. housing market and individual homeowner are still being supported by the Federal Reserve Board and U.S. government. How many more homeowners would have been foreclosed upon if the great U.S. housing bailout effort was not still ongoing?

Point being, instead of dissecting and becoming enraged by the decisions of homeowners which in many cases mirrored the decisions made on Wall Street - it has become much easier to pluck sentimental strings and attack the supposed Machiavellian maestros on Wall Street. Quite frankly, this rage directed at Wall Street has become so wildly pervasive that it necessitates a contrarian response.

Be it Wall Street, Greenspan, politicians, money managers, or even homeowners, there are plenty of parties to blame for the financial crisis. However, given that the blame game is still alive when it comes to dissecting the Great Depression, why bother? In other words, why waist time casting aspersions on those players who were operating out of a play book that our regulators at least implicitly sanctioned? The bankers paraded in front of the cameras last week should not be treated as convictable criminals. However, the regulators that failed and are failing to fight for real change should be.

BWillett@fallstreet.com

|

|

{kind=link}