|

| Log out |

|

|

|

August 23, 2006

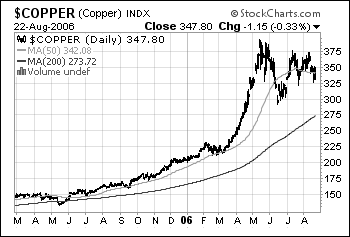

Beyond the startling fact that a nearly 30-year downtrend in copper has been completely reversed in less than 2-years, the point to be taken from Citigroups research is that although super cycles have tended to last a longtime, they also bring with them a great deal of short term price volatility. As the highs and lows during the two previous super cycles aptly demonstrate, buying at the wrong time could see your investment return very little over the long-term.

The Up-Cycle of Speculation Continues A few years ago back when gold was a screaming buy below $300 an ounce the case for owning commodities could be easily expressed. Commodities are hated and loathed right now by conventional investors. Commodities are out of favor. Commodities are not sexy. Commodities are not lusted after at the moment. Capital has abandoned commodities. It is enough to warm the contrarian heart! Zeal, 2001. In hindsight, even as recently as December 2004 when Rogers published Hot Commodities - the commodities story was just starting to hit the mainstream as funds began to rush in (I use the term in hindsight because in 2004 there was also reason to believe that the boom in commodities was going to take a breather. Indeed, even Mr. Rogers was forecasting a hard landing in China and a cooling off period in commodities in late 2004). But alas, with the commodities bull running wild for much of the last year capital has been gravitating to markets like copper and nickel for the wrong reasons. Quite frankly, that China has an insatiable thirst for commodities is no longer an undiscovered long-term investment platform so much as the catch phrase of thrill seekers trying to profit off of the next swing higher. The super cycle speculators continue to say that so long as the fundamentals are positive no price is too high, and, for the most part, they continue to be right. But eventually prices will prove too high and many latecomers will be crushed. Jim Rogers may not think that this day is coming soon, but others including Buffett and Miller are not so sure. One thing is for sure: if market rigging is not enough to stop the super cycle speculators in a market like nickel, it will take a change in the fundamentals to bring about a price correction. In the case of copper, and notwithstanding the unknowable changes in Chinas SRB stocks, demand (roughly inline with supply in 2006) is threatening to stall as the global economy slows down. The danger here is that any fundamentally driven correction could ignite a large pool of money to run to the exits en masse. As for the regulators, their message is clear: you can freely invest in anything so long as it is not something that is in short supply, you do not hoard, and your investment does not infringe upon the supposedly noble regulatory pursuit of not allowing contracts to be default on. Who or what has the bravado to short nickel anyway? 1. NYMEX has a history of raising margin requirements on silver or gold when prices are booming. Not many people would call this market rigging (largely because so few analysts focus on contract changes reported by commodity futures exchanges). Nevertheless, the conspiratorial eye cannot help but notice that when COMEX margin rates are being raised the commercials are usually extremely short while smaller investors are extremely long. Up until last year - when gold/silver broke free from COT a hike in margin requirements usually meant a falling price of gold or silver. Meaning smaller investors (who need margin) scrambled for cover while the commercials calmly locked in profits. |

||||

{kind=link}