| Log out |

|

|

|

|

April 24, 2006 |

||||||

|

Last week was one of the most exciting in a long time. With 34% of S&P 500 companies expected to report earnings on tap and a raft of potentially market moving economic reports due out, this week should be no different.

For the first time since being hammered in early 2004, the small specs also waded back into silver last week. To reiterate, although these numbers are dated, they nonetheless suggest that the party is near an end, especially since the small specs are arriving just as the commercials are in desperate need of some weak hands to try and shake out.

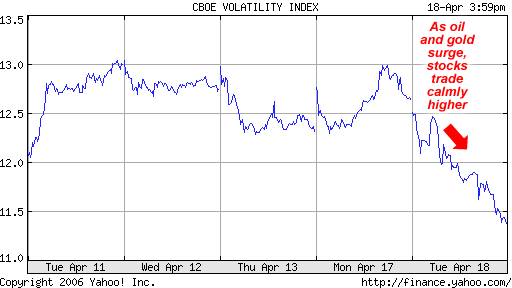

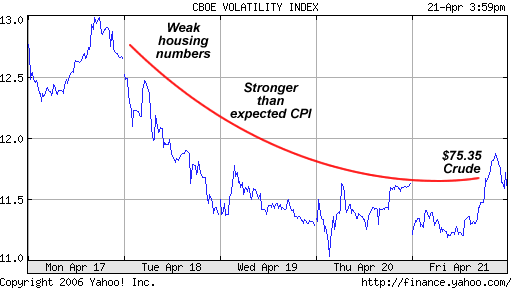

What about the once in a lifetime precious metals short covering spree that ends with financial chaos, defaults, and the destruction of the US dollar? Well, lease rates didnt jump higher last week, the commercials were only temporarily spooked, and a dramatic sell-off mid-week suggests that the mad rush into gold/silver is currently taking a pause. In light of these events, the speculation can be made that precious metals will require another event to reach higher highs. The events to watch are oil, Iran, and USD Stocks focus on the positives The Dow Jones Industrial Average reached a 6-year high last week and the Russell 2000 reached a new all-time. Better than expected earnings and dovish Fed Minutes were supposedly responsible for last weeks equity gains. However, what remains unexplained is the precipitous decline in volatility before the Fed minutes were released. Notwithstanding the softer than expected PPI report, it is almost as if someone was front running the minutes.

Being less than 400-points away from an all-time high, it is certainty possible that the Dow could defy gravity a little while longer. However, if new highs and/or investor giddiness do not arrive soon as in the next couple of weeks there is reason to believe that the markets will, at best, stagnate into the summer. Quite frankly, the potential pitfalls US stocks face are numerous including rising oil/commodity prices, a softening housing market, and interest rate/US dollar uncertainty while one of the few positives is corporate earnings growth. Investor hope for a soft landing could also be called a positive, although it is difficult to seriously contend that any economic landing can somehow translate into a quick takeoff given how reliant the US consumer has become on rising housing prices and debt. Seasonal Slow-Downs & The Threat of Market Rotation From May 2005-October 2005 mutual funds that focus primarily on American stocks attracted $6.19 billion in new money. In November 2005 alone these same funds attracted $9.23 billion. Suffice to say, it is difficult to speculate that stocks can gather momentum from May to October during a trouble free year, much less a year with the uncertainties noted above. Along with seasonal considerations, the threat of economic slow down and declining inflows into stocks could soon combine to bring back the dreaded days of stock market rotation speculation. Many on Wall Street get paid quite well to flush out seemingly cogent theories about where stock market money will move to next (we are starting to see tech/non tech speculations today, and the small/big debate is already on). However, increased speculation of rotationary forces returning to US stocks is a potential sign of a market top and/or looming bear market. This is not to say that certain sectors/industries will not perform better than others through out the business cycle (i.e. compare energy to consumer discretionary), only that when equity classes start falling The Street will ignore this negative and focus solely on whatever is rising. This is exactly what happened during 2000, months before the bear finally arrived. In short, when all US stocks stop floating higher beware.

US dollar volatility returned over the weekend and global stocks markets declined sharply. And yes, copper hit another record high in Asia overnight. To reiterate, exciting days! Even more exciting will the days be once stocks climb out of their shell and see the dangers that abound.

|

||||||